Data Dictionary

There are multiple variables in the dataset: divided in 3 categories:

Demographic information about customers

customer_id - Customer id

vintage - Vintage of the customer with the bank in number of days

age - Age of customer

gender - Gender of customer

dependents - Number of dependents

occupation - Occupation of the customer

city - City of customer (anonymised)

Customer Bank Relationship

customer_nw_category - Net worth of customer (3:Low 2:Medium 1:High)

branch_code - Branch Code for customer account

days_since_last_transaction - No of Days Since Last Credit in Last 1 year

Transactional Information

current_balance - Balance as of today

previous_month_end_balance - End of Month Balance of previous month

average_monthly_balance_prevQ - Average monthly balances (AMB) in Previous Quarter

average_monthly_balance_prevQ2 - Average monthly balances (AMB) in previous to previous quarter

current_month_credit - Total Credit Amount current month

previous_month_credit - Total Credit Amount previous month

current_month_debit - Total Debit Amount current month

previous_month_debit - Total Debit Amount previous month

current_month_balance - Average Balance of current month

previous_month_balance - Average Balance of previous month

churn - Average balance of customer falls below minimum balance in the next quarter (1/0)

Churn Prediction using Logisitic Regression

Now, that I understand the dataset in detail. It is time to build a logistic regression model to predict the churn. I have included the data dictionary above for reference.

Load Data & Packages for model building & preprocessing

Preprocessing & Missing value imputation

Select features on the basis of EDA Conclusions & build baseline model

Decide Evaluation Metric on the basis of business problem

Build model using all features & compare with baseline

Use Reverse Feature Elimination to find the top features and build model using the top 10 features & compare

Loading Packages

import numpy as np

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

from sklearn.preprocessing import LabelEncoder

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import KFold, StratifiedKFold, train_test_split

from sklearn.metrics import roc_auc_score, accuracy_score, confusion_matrix, roc_curve, precision_score, recall_score, precision_recall_curve

import warnings

warnings.simplefilter(action='ignore', category=FutureWarning)

warnings.simplefilter(action='ignore', category=UserWarning)

Loading Data

df_churn = pd.read_csv('bank_customer_data.csv') |

Missing Values

Before I go on to build the model, I must look for missing values within the dataset as treating the missing values is a necessary step before I fit a logistic regression model on the dataset.

pd.isnull(df_churn).sum() customer_id 0

vintage 0

age 0

gender 525

dependents 2463

occupation 80

city 803

customer_nw_category 0

branch_code 0

days_since_last_transaction 3223

current_balance 0

previous_month_end_balance 0

average_monthly_balance_prevQ 0

average_monthly_balance_prevQ2 0

current_month_credit 0

previous_month_credit 0

current_month_debit 0

previous_month_debit 0

current_month_balance 0

previous_month_balance 0

churn 0

dtype: int64 |

The result of this function shows that there are quite a few missing values in columns gender, dependents, city, days since last transaction and Percentage change in credits. I go through each of them 1 by 1 to find the appropriate missing value imputation strategy for each of them.

Gender For a quick recall look at the categories within gender column

df_churn['gender'].value_counts() Male 16548

Female 11309

Name: gender, dtype: int64 |

So there is a good mix of males and females and arguably missing values cannot be filled with any one of them. I could create a seperate category by assigning the value -1 for all missing values in this column.

Before that, first I will convert the gender into 0/1 and then replace missing values with -1

#Convert Gender dict_gender = {'Male': 1, 'Female':0} df_churn.replace({'gender': dict_gender}, inplace = True) df_churn['gender'] = df_churn['gender'].fillna(-1) |

Dependents, occupation and city with mode

Next I will have a quick look at the dependents & occupations column and impute with mode as this is sort of an ordinal variable

df_churn['dependents'].value_counts() 0.0 21435

2.0 2150

1.0 1395

3.0 701

4.0 179

5.0 41

6.0 8

7.0 3

9.0 1

52.0 1

36.0 1

50.0 1

8.0 1

25.0 1

32.0 1

Name: dependents, dtype: int64 |

df_churn['occupation'].value_counts()

self_employed 17476

salaried 6704

student 2058

retired 2024

company 40

Name: occupation, dtype: int64

df_churn['dependents'] = df_churn['dependents'].fillna(0)

df_churn['occupation'] = df_churn['occupation'].fillna('self_employed')

Similarly City can also be imputed with most common category 1020

df_churn['city'] = df_churn['city'].fillna(1020) |

Days since Last Transaction

A fair assumption can be made on this column as this is number of days since last transaction in 1 year, I can substitute missing values with a value greater than 1 year say 999

df_churn['days_since_last_transaction'] = df_churn['days_since_last_transaction'].fillna(999) |

Preprocessing

Now, before applying linear model such as logistic regression, I need to scale the data and keep all features as numeric strictly.

Dummies with Multiple Categories

# Convert occupation to one hot encoded features df_churn = pd.concat([df_churn,pd.get_dummies(df_churn['occupation'],prefix = str('occupation'),prefix_sep='_')],axis = 1) |

Scaling Numerical Features for Logistic Regression

Now, I remember that there are a lot of outliers in the dataset especially when it comes to previous and current balance features. Also, the distributions are skewed for these features if you recall from the EDA. I will take 2 steps to deal with that here:

Log Transformation

Standard Scaler

Standard scaling is anyways a necessity when it comes to linear models and I have done that here after doing log transformation on all balance features.

num_cols = ['customer_nw_category', 'current_balance', 'previous_month_end_balance', 'average_monthly_balance_prevQ2', 'average_monthly_balance_prevQ', 'current_month_credit','previous_month_credit', 'current_month_debit', 'previous_month_debit','current_month_balance', 'previous_month_balance'] for i in num_cols: df_churn[i] = np.log(df_churn[i] + 17000) std = StandardScaler() scaled = std.fit_transform(df_churn[num_cols]) scaled = pd.DataFrame(scaled,columns=num_cols) |

df_df_og = df_churn.copy() df_churn = df_churn.drop(columns = num_cols,axis = 1) df_churn = df_churn.merge(scaled,left_index=True,right_index=True,how = "left") |

y_all = df_churn.churn df_churn = df_churn.drop(['churn','customer_id','occupation'],axis = 1) |

Model Building and Evaluation Metrics

Since this is a binary classification problem, I could use the following 2 popular metrics:

Recall

Area under the Receiver operating characteristic curve

Now, I am looking at the recall value here because a customer falsely marked as churn would not be as bad as a customer who was not detected as a churning customer and appropriate measures were not taken by the bank to stop him/her from churning The ROC AUC is the area under the curve when plotting the (normalized) true positive rate (x-axis) and the false positive rate (y-axis). My main metric here would be Recall values, while AUC ROC Score would take care of how well predicted probabilites are able to differentiate between the 2 classes.

Conclusions from Exploratory Data Analysis (EDA)

For debit values, I see that there is a significant difference in the distribution for churn and non churn and it might be turn out to be an important feature

For all the balance features the lower values have much higher proportion of churning customers

For most frequent vintage values, the churning customers are slightly higher, while for higher values of vintage, I have mostly non churning customers which is in sync with the age variable

I see significant difference for different occupations and certainly would be interesting to use as a feature for prediction of churn.

Now, I will first split my dataset into test and train and using the above conclusions select columns and build a baseline logistic regression model to check the ROC-AUC Score & the confusion matrix

Baseline Columns

baseline_cols = ['current_month_debit', 'previous_month_debit','current_balance','previous_month_end_balance','vintage' ,'occupation_retired', 'occupation_salaried','occupation_self_employed', 'occupation_student'] |

df_baseline = df_churn[baseline_cols] |

Train Test Split to create a validation set

# Splitting the data into Train and Validation set xtrain, xtest, ytrain, ytest = train_test_split(df_baseline,y_all,test_size=1/3, random_state=11, stratify = y_all) |

model = LogisticRegression() model.fit(xtrain,ytrain) pred = model.predict_proba(xtest)[:,1] |

AUC ROC Curve & Confusion Matrix

from sklearn.metrics import roc_curve fpr, tpr, _ = roc_curve(ytest,pred) auc = roc_auc_score(ytest, pred) plt.figure(figsize=(12,8)) plt.plot(fpr,tpr,label="Validation AUC-ROC="+str(auc)) x = np.linspace(0, 1, 1000) plt.plot(x, x, linestyle='-') plt.xlabel('False Positive Rate') plt.ylabel('True Positive Rate') plt.legend(loc=4) plt.show() |

|

# Confusion Matrix pred_val = model.predict(xtest) |

label_preds = pred_val cm = confusion_matrix(ytest,label_preds) def plot_confusion_matrix(cm, normalized=True, cmap='bone'): plt.figure(figsize=[7, 6]) norm_cm = cm if normalized: norm_cm = cm.astype('float') / cm.sum(axis=1)[:, np.newaxis] sns.heatmap(norm_cm, annot=cm, fmt='g', xticklabels=['Predicted: No','Predicted: Yes'], yticklabels=['Actual: No','Actual: Yes'], cmap=cmap) plot_confusion_matrix(cm, ['No', 'Yes']) |

|

# Recall Score recall_score(ytest,pred_val) |

0.11580148317170565 |

Cross validation

Cross Validation is one of the most important concepts in any type of data modelling. It simply says, try to leave a sample on which you do not train the model and test the model on this sample before finalizing the model.

I divide the entire population into k equal samples. Now I train models on k-1 samples and validate on 1 sample. Then, at the second iteration I train the model with a different sample held as validation.

In k iterations, I have basically built the model on each sample and held each of them as validation. This is a way to reduce the selection bias and reduce the variance in prediction power.

Since it builds several models on different subsets of the dataset, I can be more certain of model performance if I use CV for testing my models.

def cv_score(ml_model, rstate = 12, thres = 0.5, cols = df_churn.columns): i = 1 cv_scores = [] df1 = df_churn.copy() df1 = df_churn[cols]

# 5 Fold cross validation stratified on the basis of target kf = StratifiedKFold(n_splits=5,random_state=rstate,shuffle=True) for df_index,test_index in kf.split(df1,y_all): print('\n{} of kfold {}'.format(i,kf.n_splits)) xtr,xvl = df1.loc[df_index],df1.loc[test_index] ytr,yvl = y_all.loc[df_index],y_all.loc[test_index]

# Define model for fitting on the training set for each fold model = ml_model model.fit(xtr, ytr) pred_probs = model.predict_proba(xvl) pp = []

# Use threshold to define the classes based on probability values for j in pred_probs[:,1]: if j>thres: pp.append(1) else: pp.append(0)

# Calculate scores for each fold and print pred_val = pp roc_score = roc_auc_score(yvl,pred_probs[:,1]) recall = recall_score(yvl,pred_val) precision = precision_score(yvl,pred_val) sufix = "" msg = "" msg += "ROC AUC Score: {}, Recall Score: {:.4f}, Precision Score: {:.4f} ".format(roc_score, recall,precision) print("{}".format(msg))

# Save scores cv_scores.append(roc_score) i+=1 return cv_scores |

baseline_scores = cv_score(LogisticRegression(), cols = baseline_cols) |

1 of kfold 5 ROC AUC Score: 0.7644836090843695, Recall Score: 0.0751, Precision Score: 0.5766 2 of kfold 5 ROC AUC Score: 0.779451238310554, Recall Score: 0.0751, Precision Score: 0.6695 3 of kfold 5 ROC AUC Score: 0.7551621478942728, Recall Score: 0.1350, Precision Score: 0.6425 4 of kfold 5 ROC AUC Score: 0.7582070977015274, Recall Score: 0.1169, Precision Score: 0.6508 5 of kfold 5 ROC AUC Score: 0.7632311004249608, Recall Score: 0.1112, Precision Score: 0.5850 |

Now I will try using all columns available to check if I get significant improvement.

all_feat_scores = cv_score(LogisticRegression()) |

1 of kfold 5 ROC AUC Score: 0.7322735587298325, Recall Score: 0.1093, Precision Score: 0.5066 2 of kfold 5 ROC AUC Score: 0.7681477751515774, Recall Score: 0.1968, Precision Score: 0.6809 3 of kfold 5 ROC AUC Score: 0.7392333107476944, Recall Score: 0.1673, Precision Score: 0.5714 4 of kfold 5 ROC AUC Score: 0.7394851378820373, Recall Score: 0.1597, Precision Score: 0.6667 5 of kfold 5 ROC AUC Score: 0.758833273580065, Recall Score: 0.1730, Precision Score: 0.5987 |

There is some improvement in both ROC AUC Scores and Precision/Recall Scores. Now I can try backward selection to select the best subset of features which give the best score.

Reverse Feature Elimination or Backward Selection

I have already built a model using all the features and a separate model using some baseline features. I can try using backward feature elimination to check if I can do better. I will do that next.

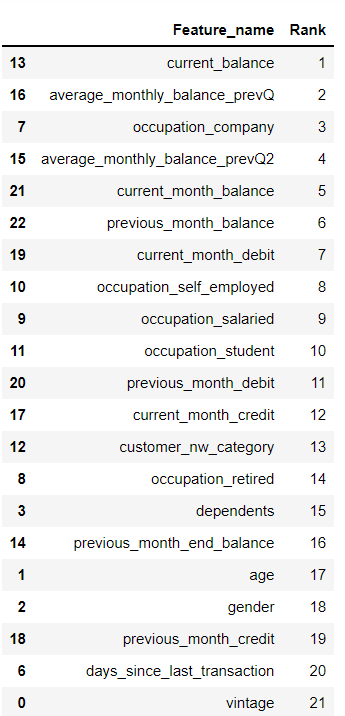

from sklearn.feature_selection import RFE import matplotlib.pyplot as plt # Create the RFE object and rank each feature model = LogisticRegression() rfe = RFE(estimator=model, n_features_to_select=1, step=1) rfe.fit(df_churn, y_all) |

RFE(estimator=LogisticRegression(), n_features_to_select=1) |

ranking_df = pd.DataFrame() ranking_df['Feature_name'] = df_churn.columns ranking_df['Rank'] = rfe.ranking_ |

ranked = ranking_df.sort_values(by=['Rank']) |

ranked |

The balance features are proving to be very important as can be seen from the table. The RFE function can also be used to select features. I selected the top 10 features from this table and checked score.

rfe_top_10_scores = cv_score(LogisticRegression(), cols = ranked['Feature_name'][:10].values) |

1 of kfold 5 ROC AUC Score: 0.7986881101633954, Recall Score: 0.2281, Precision Score: 0.7362 2 of kfold 5 ROC AUC Score: 0.8050442914397288, Recall Score: 0.2234, Precision Score: 0.7556 3 of kfold 5 ROC AUC Score: 0.7985130070256687, Recall Score: 0.2205, Precision Score: 0.7250 4 of kfold 5 ROC AUC Score: 0.7935095616193245, Recall Score: 0.2120, Precision Score: 0.7360 5 of kfold 5 ROC AUC Score: 0.7942222838028076, Recall Score: 0.1911, Precision Score: 0.6745 |

Wow, the top 10 features obtained using the reverse feature selection are giving a much better score than any of our earlier attempts. This is the power of feature selection and it especially works well in case of linear models as tree based models are in itself to some extent capable of doing feature selection.

The recall score here is quite low. I should play around with the threshold to get a better recall score. AUC ROC depends on the predicted probabilities and is not impacted by the threshold. I will try 0.2 as threshold which is close to the overall churn rate

cv_score(LogisticRegression(), cols = ranked['Feature_name'][:10].values, thres=0.14) |

1 of kfold 5 ROC AUC Score: 0.7986881101633954, Recall Score: 0.8308, Precision Score: 0.2836 2 of kfold 5 ROC AUC Score: 0.8050442914397288, Recall Score: 0.8375, Precision Score: 0.2902 3 of kfold 5 ROC AUC Score: 0.7985130070256687, Recall Score: 0.8279, Precision Score: 0.2897 4 of kfold 5 ROC AUC Score: 0.7935095616193245, Recall Score: 0.8213, Precision Score: 0.2840 5 of kfold 5 ROC AUC Score: 0.7942222838028076, Recall Score: 0.8108, Precision Score: 0.2927 |

[0.7986881101633954, 0.8050442914397288, 0.7985130070256687, 0.7935095616193245, 0.7942222838028076] |

I observe that there is continuous improvement in the Recall Score. However, clearly precision score is going down. On the basis of business requirement the bank can take a call on deciding the threshold. Without knowing the metrics relevant to the business, the best course of action is to optimize for AUC ROC Score so as to find the best probabilities here.

コメント